Updated: Oct 14, 2024, 10:54am

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors’ opinions or evaluations.

The best small business loans can help you fund your venture with rates and terms that work for you. We compared 25 lenders to find the best options available, including business term loans, business lines of credit, merchant cash advances and others. The highest-rated lenders offer loan amounts over $500,000 and have flexible qualification requirements.

Best Business Loans of October 2024

Best for Fast Business Loans

QuickBridge

APR range

Factor rates start at 1.11

Factor rates start at 1.11

Editor’s Take

QuickBridge provides small business loans and equipment financing to businesses in all 50 states.

Why We Like It

QuickBridge can fund loans within 24 hours for borrowers with fair to excellent credit and offers flexible repayment options.

What We Don’t Like

Maximum loan amounts are smaller than what other lenders offer, and the minimum annual revenue requirements can make a loan from QuickBridge difficult to qualify for.

Who It’s Best For

The lender is attractive to business owners who need short-term loans with a quick funding turnaround.

Pros & Cons

- Flexible repayment options

- Quick application and fast funding deposited to a bank account

- Early payoff discounts

- Loan interest may be high

- $250,000 minimum annual revenue requirement for small business loans

- Only short-term repayment terms are available

Details

Eligibility

- Minimum credit score: 600

- Time in business: six months

- Minimum revenue: $250,000 per year

Turnaround time

You can apply and receive a decision from QuickBridge on the same day.

Best for Business Lines of Credit

American Express® Business Line of Credit*

Minimum Credit Score

660 FICO at the time of application

660 FICO at the time of application

Editor’s Take

The American Express® Business Line of Credit* gives business owners access to a range of line of credit options. Monthly fees vary depending on the financing term.

All businesses are unique and are subject to approval and review.

Why We Like It

The American Express® Business Line of Credit* offers business owners lines of credit from $2,000 to $250,000 and repayment terms include six, 12, 18 and 24 months (with fees of 3% to 9% for six-month loans, 6% to 18% for 12-month loans, 9% to 27% for 18-month loans and 12% to 18% for 24-month loans).

What We Don’t Like

American Express® Business Line of Credit* can take up to three days to fund and has requirements that may be difficult for newly formed businesses to reach.

Who It’s Best For

With flexible repayment options, the American Express® Business Line of Credit* is best for businesses looking for short-term business lines of credit with transparent costs.

Pros & Cons

- No prepayment penalty

- Four different repayment options

- Offers small to large lines of credit

- Monthly fees on unpaid balances

- Requires personal guarantee

- Lines of credit over $150,000 are only available to borrowers who meet additional criteria

Details

Eligibility

- Minimum credit score: 660 FICO at the time of application

- Time in business: At least one year

- Average revenue: at least $3,000 monthly

All businesses are unique and are subject to approval and review. The required FICO score may be higher based on your relationship with American Express, credit history and other factors.

Turnaround time

Once application is approved, funds can take up to three business days to appear in your account, depending on your bank.

*American Express® Business Line of Credit offers two loan types, installment loans and single repayment loans for eligible borrowers. All loan term types, loan term lengths, and pricing are subject to eligibility requirements, application, and final approval.

This [content / article] contains general information about the American Express® Business Line of Credit installment loan type only.

Best for Startup Funding

Fundbox

APR range

Interest rates start at 4.66%

Interest rates start at 4.66%

Editor’s Take

Fundbox is an alternative lender that offers short-term lines of credit and business loans. Startups that need money in a pinch can also rely on Fundbox to provide business loan decisions in just three minutes and next-business-day funding.

Why We Like It

Fundbox offers flexible qualification requirements, including a minimum time in business of six months and an annual revenue requirement of $100,000.

What We Don’t Like

Loans from Fundbox range from , which may not be enough for some businesses.

Who It’s Best For

With a short time in business requirement, low minimum credit score and low annual revenue requirement, Fundbox is best for startups and other newly established businesses.

Pros & Cons

- No prepayment penalty

- Low minimum annual revenue requirement

- Next-business-day funding

- Only short-term repayment terms are available

- Does not disclose APRs

Details

Eligibility

- Minimum credit score: 600

- Time in business: Six months

- Minimum revenue: $100,000 per year

Turnaround time

With a business line of credit from Fundbox, you can receive your funds as soon as the next business day.

Best for Short-Term Business Loans

OnDeck

Editor’s Take

OnDeck is an online lender that offers both lines of credit and loans to businesses in all states except North Dakota.

Why We Like It

OnDeck gives business owners the option between term loans and lines of credit with a range of repayment terms. Lines of credit are available with short repayment terms of 12, 18 or 24 months, and OnDeck’s term loan is available with repayment terms of up to 24 months.

What We Don’t Like

With small loan amounts and short repayment terms, financing from OnDeck may not be the best option for every business.

Who It’s Best For

OnDeck’s loans can be a great financing option for businesses that want short-term loans and to minimize interest costs.

Pros & Cons

- Term loans from $5,000 to $250,000

- Lines of credit from $6,000 to $100,000

- Same-day funding

- Low minimum credit score requirement

- $100,000 minimum annual revenue requirement

- Must have been operating for at least one year

- Does not lend to businesses in North Dakota

Details

Eligibility

- Minimum credit score: 625

- Time in business: One year

- Minimum revenue: $100,000 per year

Turnaround time

You can apply and receive a decision from OnDeck on the same day.

Best for Business Lines of Credit From a Bank

Wells Fargo Business Line of Credit

APR range

Prime + 1.75% to prime + 9.75%

Prime + 1.75% to prime + 9.75%

Editor’s Take

Wells Fargo, with physical branches across the country, offers business lines of credit and term loans. It offers $10,000 to $150,000 through its BusinessLine line of credit, which you can apply for in person or online.

Why We Like It

For borrowers who are looking for financing from an established bank with physical branches, Wells Fargo stands out. The lender has large lines of credit, and it also offers its Prime business line of credit for established businesses with a limit of up to $1 million.

What We Don’t Like

Wells Fargo has stringent qualification requirements for its line of credit and also requires a personal guarantee.

Who It’s Best For

Wells Fargo is best for businesses that are looking for a lender with physical branches and that operate in a state where the bank has locations.

Pros & Cons

- Offers physical branch locations

- Available in all 50 states

- Transparent loan costs

- Annual fee after first year

- Requires at least two years in business

- Requires personal guarantee

Details

Eligibility

- Minimum credit score: 680

- Time in business: Two years

- Minimum revenue: Does not disclose

Turnaround time

Wells Fargo does not disclose its approval and funding turnaround time.

Best for Large Business Loans

Fora Financial Business Loans

Editor’s Take

Fora Financial is an online business loan lender that offers both term loans and revenue advances. Revenue advances are similar to merchant cash advances (MCAs) but use total sales revenue instead of credit card sales.

Why We Like It

Fora Financial offers large business loans of up to $1.5 million, which is over five times more than most lenders on our list. Not only does it offer high loan amounts, but it also gives you the opportunity to increase your loan amount after you pay at least 60% of the original loan.

What We Don’t Like

Although Fora Financial offers large business loans and revenue advance amounts, the term lengths of up to 18 months are shorter than what other lenders offer.

Who It’s Best For

Fora Financial is best for businesses that are looking to finance large sums or are looking for large revenue advances.

Pros & Cons

- Large loan amounts of up to $1.5 million

- Low minimum credit score requirement

- Offers prepay discounts

- Short repayment terms of up to 18 months

- Funding is slower than competitor lenders on our list

- Daily or weekly repayments

Details

Eligibility

- Minimum credit score: 570

- Time in business: Six months

- Minimum revenue: $20,000 in monthly revenue per month

Turnaround time

Fora Financial offers approvals within 24 hours and funding within 72 hours.

Best for Robust Financing Options

National Funding

Editor’s Take

National Funding offers short-term working capital loans and equipment financing. The loans are available in terms of four months to two years, paid daily or weekly.

Why We Like It

We picked National Funding because it offers robust financing options for small to midsized businesses. Working capital loans are available from $5,000 to $500,000 and also equipment financing up to $150,000.

What We Don’t Like

National Funding’s financing options require daily or weekly payments, and to qualify, businesses must have minimum gross annual sales of $250,000.

Who It’s Best For

National Funding is best for newly established businesses with high gross sales that are looking for various funding options to finance their business.

Pros & Cons

- Financing up to $500,000

- Early payoff discounts

- Most loans are funded within 24 hours of approval

- Requires daily or weekly payments

- Potentially high borrowing costs

- Requires minimum gross annual sales of $250,000

Details

Eligibility

- Minimum credit score: 600 (575 for equipment financing)

- Time in business: Six months

- Minimum sales: $250,000 per year

Turnaround time

Most loans are funded within 24 hours of approval, subject to receipt of required documentation, underwriting guidelines and processing time by your bank.

Best for Flexible Line of Credit Repayment Terms

Bluevine

APR range

Simple interest starts at 7.8%

Simple interest starts at 7.8%

Editor’s Take

Bluevine is an online lender that offers short-term business lines of credit. Bluevine’s financing can be funded as soon as the same day.

Why We Like It

We picked Bluevine for its line of credit which ranges from $5,000 to $250,000 and can be repaid with a weekly or monthly structure. Customers who repay weekly make payments each week over 26 weeks, while customers who repay monthly make payments each month over one year.

What We Don’t Like

Bluevine’s business line of credit requires a high minimum annual revenue and isn’t available in all 50 states.

Who It’s Best For

Bluevine is best for businesses that are looking for a short-term line of credit with flexible repayment options.

Pros & Cons

- Receive a decision within five minutes and instant funding with a Bluevine business checking account, or receive funds within 24 hours

- Lines of credit up to $250,000

- Low credit score requirement

- No mobile app for its line of credit

- Monthly revenue requirement

- Not available to businesses in Nevada, North Dakota, South Dakota, Puerto Rico and other U.S. territories

Details

Eligibility

Eligibility varies on the specific program a business owner chooses.

Weekly plan

- Minimum credit score: 625

- Time in business: Less than one year

- Minimum revenue: $10,000 monthly or $120,000 annually

- Business type: Corporation or LLC

- Bankruptcies: No past bankruptcies

Monthly plan

- Minimum credit score: 700

- Time in business: Three years

- Minimum revenue: $80,000 per month or $960,000 annually

- Business type: Corporation or LLC

Turnaround time

After you submit your application, you can receive a decision in as quickly as five minutes and instant funding with a Bluevine business checking account. Borrowers who don’t have a Bluevine business checking account can receive funds within 24 hours.

Best for Merchant Cash Advances

Biz2Credit

Loan amounts

up to $1 million

Revenue-based financing. Varies depending on product and qualifications

Minimum Credit Score

650*

*See website for details

up to $1 million

Revenue-based financing. Varies depending on product and qualifications

650*

*See website for details

Editor’s Take

Biz2Credit is an online lender that offers revenue-based financing and term loans. The lender says its revenue-based financing is its most popular product, and the average funding amount in 2023 was over $92,000.

Why We Like It

Biz2Credit offers revenue-based financing to businesses with at least $10,000 in annual revenue.

What We Don’t Like

Biz2Credit doesn’t disclose financing costs or the turnaround time for revenue-based financing.

Who It’s Best For

With flexible qualification requirements, Biz2Credit’s revenue-based financing can be best for new businesses or businesses that may not qualify for financing elsewhere.

Pros & Cons

- Revenue-based financing has flexible qualification requirements

- Can pre-qualify for submitting an application

- Offers term loans with weekly or biweekly payments

- Does not disclose financing costs

- Does not disclose turnaround time

- High annual revenue requirement

Details

Eligibility

Eligibility varies based on the financing option you choose.

Term loan

- Minimum credit score: 650

- Time in business: 18 months

- Minimum revenue: $250,000 per year

Revenue-based financing

- Minimum credit score: 575

- Time in business: 6 months

- Minimum revenue: $10,000 per year

Turnaround time

Biz2Credit does not disclose the turnaround time for its financing options.

Best for Long-Term Business Loans

Funding Circle

Editor’s Take

Funding Circle is a peer-to-peer marketplace lender that connects businesses with financing. The lender offers a simple application process and funding in as little as 48 hours.

Why We Like It

Funding Circle stands out for its long-term business loans with terms of up to seven years for established businesses. This is much longer than most other lenders.

What We Don’t Like

Funding Circle’s loans come with an origination fee of at least 3.49% and require at least two years in business.

Who It’s Best For

Funding Circle’s business financing is best for established businesses that need to spread loan payments over a long period.

Pros & Cons

- Loans from $25,000 to $500,000

- Funding in as little as 48 hours

- No minimum annual revenue requirement for most loans

- One-time origination fee between 3.49% to 6.99% of the approved loan amount

- Requires two years in business, so it’s not ideal for startups

- Not available to Nevada businesses

Details

Eligibility

- Minimum credit score: 660 for most loans; 650 for SBA loans

- Time in business: Two years

- Minimum revenue: None for most loans; $400,000 per year for SBA loans

Turnaround time

Depending on the loan type, you can receive your funds within two days. However, SBA loan funding may take up to two weeks.

Summary: Best Small Business Loans Of October 2024

Featured Partner Offer

Funding amounts

Up to $1 million

Revenue-based financing. Varies depending on product and qualifications

Minimum credit score

650*

*See website for details

Time in business

12 months+*

*See website for details

Tips for Comparing Small Business Loans

Consider these tips when comparing small business loans:

Review Qualification Requirements

Prequalify Where Possible

Determine How You Want To Receive Your Funds

Consider the Repayment Terms and Flexibility

Understand Underwriting and Funding Speeds

Look Out for Additional Fees

Evaluate the Lender’s Customer Support Options

What should business owners consider when choosing a small business loan?

Tom Thunstrom

Advisory Board Member

Taylor Medine

Mortgages & Loans Writer

Colin Beresford

Mortgages & Loans Editor

When considering a small business loan, consider these factors:

- What do you need the funds for? If you need money for cash flow, a line of credit is probably your best bet. A line of credit provides a cash infusion that can be repaid once business conditions improve. If you need money for physical assets, whether it be new facilities or new equipment, a loan backed by those assets will provide a lower rate and reasonable terms.

- If your business is struggling or starting up, you may be able to qualify for an SBA-backed loan. Most lenders will require some form of a business plan and financial projections to help them understand what you need the funds for and how you’ll be able to repay the debt. If you are unsure where to begin on a business plan, you can reach out to SCORE, the Women’s Business Center, or the SBDC, all of whom can help you at no cost.

- Make sure you ask about prepayment penalties and whether your interest rate is adjustable. An adjustable rate can impact the amount of principal you pay on a loan and possibly the balloon payment, if any, at the end of a loan repayment period.

Neighborhood banks offer the best rates on business loans—but usually for borrowers with years in the business game and good credit. What if your business doesn’t yet fit into this category? All isn’t lost.

Check out online lenders. Some offer lenient credit and revenue requirements for startups and smaller operations.

To find the most affordable loan, take some time to prequalify for several loans. This way, you’re better positioned to compare interest rates, fees, monthly payments and long-term costs.

When you’re considering a business loan, it can be worthwhile to understand all of your options before going forward with financing. Business loan lenders offer a variety of products, so finding the financing that works for your business can put you in the best possible position to repay your debt.

How Do Small Business Loans Work?

Small business loans help companies make large purchases and cover the cost of doing business. Loans generally are issued as a lump sum that can be used to make a specific purchase or manage cash flow and then repaid with interest. However, there are other types of small business loans—like lines of credit, merchant cash advances and invoice financing—that can be used to access cash more quickly and on an as-needed basis.

The best loan for a business depends on a number of factors, including its creditworthiness, how much it needs to borrow, what the funds will be used for and how quickly it needs access to loan proceeds.

Read More: How Do Business Loans Work?

Common Types of Small Business Loans

In general, small business loans help businesses access the money they need to operate and grow. However, there are several types of small business loans, and it’s important to find the best fit for your needs.

SBA Loans

Term Loans

Lines of Credit

Invoice Factoring and Financing

Merchant Cash Advances

Equipment Financing

Commercial Real Estate Loans

Bank Loans

Find the Best Startup Business Loans of 2024

Pros and Cons of Small Business Loans

A small business loan isn’t right for every venture. Before going forward with this financing, consider the pros and cons:

Pro Tip

If feasible, consider asking a friend or family member with good credit to co-sign the loan. A co-signer’s good credit can positively impact your loan terms and increase the likelihood of approval.

Best Place To Get a Business Loan

Small business loans are available from a variety of traditional banks and credit unions as well as online lenders. However, each lender is limited by its own financial products and lending requirements.

1. Banks & Credit Unions

2. Online Lenders

Related: Best Same-Day Business Loans

How To Qualify for a Business Loan

The requirements for small business loans can vary by lender. But in general, lenders may review the following information to approve you for a loan:

- Personal credit. You may be able to qualify for a business loan with a credit score as low as 500. However, a good score of at least 670 could give you a better shot at getting approved for a competitive rate.

- Time in business. Lenders typically require that you be in business for at least six months to two years to qualify for a loan.

- Business checking accounts. Lenders may require that you have a business checking account with several months of transactions to show cash flow.

- Business revenue. Most lenders require that you have between $100,000 to $250,000 annual business revenue to qualify.

How To Get a Small Business Loan in 5 Steps

The business loan application and underwriting process varies by lender, but most banks and lenders follow the same general guidelines. To get a small business loan, expect to follow these general steps:

- Determine the type of loan you need. Some lenders limit what industries they’ll finance or how loan funds may be used, so determine how you’ll use the cash before applying for a loan. Also evaluate how much you need to borrow, as this may impact the type of loan you apply for and the best lenders to approach for funds.

- Familiarize yourself with your credit profile. Lenders typically look at a business owner’s personal credit score when evaluating a loan application. You should have a score of at least 680 to qualify for an SBA loan or a traditional bank loan, and 630 for equipment financing or business lines of credit. Short-term financing and merchant cash advances typically have less stringent requirements—averaging around 600 and 550, respectively.

- Research lenders. When shopping for a small business loan, determine whether your current bank offers small business loans that meet your needs. This can streamline the application process because the bank will already have your financial information on file. Next, research other banks, credit unions and online lenders to compare available loan amounts, repayment terms and rates.

- Gather required documentation. Required documentation varies by lender. However, most lending institutions require a business plan, at least 12 months of personal and business bank statements, tax returns for at least two years and details about any current and past business loans. Lenders also require copies of applicable business licenses and legal documents, details about available collateral and a description of how loan proceeds will be used.

- Submit a formal loan application. Once you research the best small business loans and prepare your business for due diligence, submit a formal loan application. The process varies by lender, so familiarize yourself with the application process and contact customer service with questions.

Pro Tip

If you don’t qualify for a business loan because of having limited time in business or lack of business credit, consider using a personal loan to finance your venture. Your personal income and credit rather than your business finances are reviewed for personal loan eligibility, which can help you get approved. Not all personal loan lenders allow borrowers to use funding for business purposes, but those that do may offer competitive interest rates and low fees to borrowers with stable income and a credit score of 700 or higher.

Survey: How Do Business Owners Use Loan Funds?

Small business financing allows borrowers to use funds for a range of purposes, often depending on the loan type. Forbes Advisor surveyed 500 borrowers to understand how business owners used their funds. The most common use was for startup costs; equipment purchases and inventory purchases closely followed.

Here’s a glance at how business loan uses stack up.

Alternatives to Small Business Loans

If a small business loan doesn’t seem right for your specific needs, consider other options to get the financing your business needs.

Business Line of Credit

Business Credit Card

Crowdfunding

Personal Loans for Business

Small Business Grants

Methodology

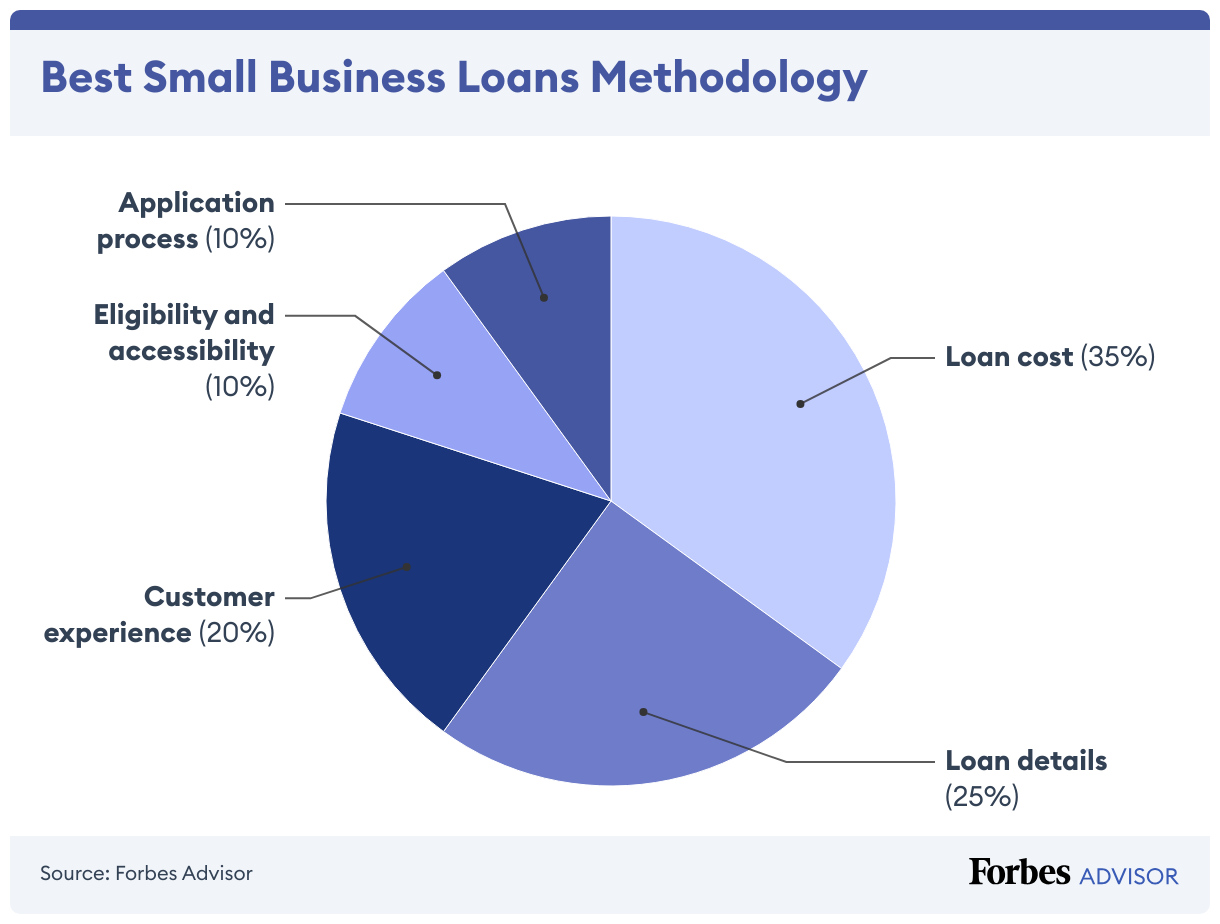

We reviewed 25 popular lenders based on 16 data points in the categories of loan details, loan costs, eligibility and accessibility, customer experience and the application process. We chose the nine best lenders based on the weighting assigned to each category:

- Loan cost. 35%

- Loan details. 25%

- Customer experience. 20%

- Eligibility and accessibility. 10%

- Application process. 10%

Within each major category, we also considered several characteristics, including available loan amounts, repayment terms and applicable fees. We also looked at minimum credit score and time in business requirements and the geographic availability of the lender. Finally, we evaluated each provider’s customer support tools, borrower perks and features that simplify the borrowing process—like online applications, prequalification options and mobile apps.

Where appropriate, we awarded partial points depending on how well a lender met each criterion.

To learn more about how Forbes Advisor rates lenders, and our editorial process, check out our Business Loans Rating Methodology.

The online survey of 500 Americans who have applied for a business loan was commissioned by Forbes Advisor and conducted by market research company OnePoll, in accordance with the Market Research Society’s code of conduct. Data was collected from July 9 to July 16, 2024. The margin of error is +/- 4.4 points with 95% confidence. This survey was overseen by the OnePoll research team, which is a member of the MRS and has corporate membership with the American Association for Public Opinion Research (AAPOR).

Frequently Asked Questions (FAQs)

What can you do if you’re denied a small business loan?

There are a number of steps you can take if you’re denied a small business loan. First, try to find out why your application was denied. If your SBA loan application is denied, you’re entitled to a notice of denial that details the reasons; you may receive this directly from the SBA or from your lender.

If, instead, you are denied a small business loan through an online lender or other financial institution, contact them to find out why you were not approved. They may be able to provide insight into how to improve your future approval odds.

Once you know why your loan application was rejected, take steps to rectify the underlying issues. For example, you may need to improve your credit score, establish more consistent sales or reassess the amount you need to borrow.

How hard is it to get a small business loan?

Getting a small business loan may prove more challenging than other financing options like business credit cards. Although qualification requirements vary by lender, most lenders typically look at the business owner’s personal credit score and the business’ annual revenue. Many lenders require a minimum personal credit score of 600 to 660 and annual revenue between $100,000 and $250,000.

We recommend confirming the qualification requirements with your preferred lender before applying.

What is the easiest way to get a small business loan?

The easiest way to get a small business loan may be through online lenders instead of traditional banks because borrower requirements may be more flexible. With an online lender, you may be able to quickly prequalify and get funding as soon as the same business day as long as you meet eligibility requirements.

How much income do you need to get a business loan?

Typically, lenders require businesses to have an annual revenue of between $100,000 and $250,000. If your business makes less than that, there are business loans for low-revenue companies that may offer funding options for your business.

¹The required FICO score may be higher based on your relationship with American Express, credit history, and other factors.

Forbes Advisor adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners.